Anderson-Rubin Confidence Intervals based on feols IV regression objects

In this vignette, we demonstrate how to compute Anderson-Rubin confidence intervals for instrumental variables regression models estimated using the feols function from the fixest package. The Anderson-Rubin method provides robust inference in the presence of weak instruments.

We will use the built-in mtcars dataset for illustration. In this example, we will regress mpg (miles per gallon) on cyl (number of cylinders) using hp (horsepower) as an endogenous regressor and qsec (1/4 mile time) as an instrument.

First, we run a regression using feols.

Second, we compute the Anderson-Rubin confidence intervals for the coefficient of the endogenous regressor hp using the ar_ci function from the arci package.

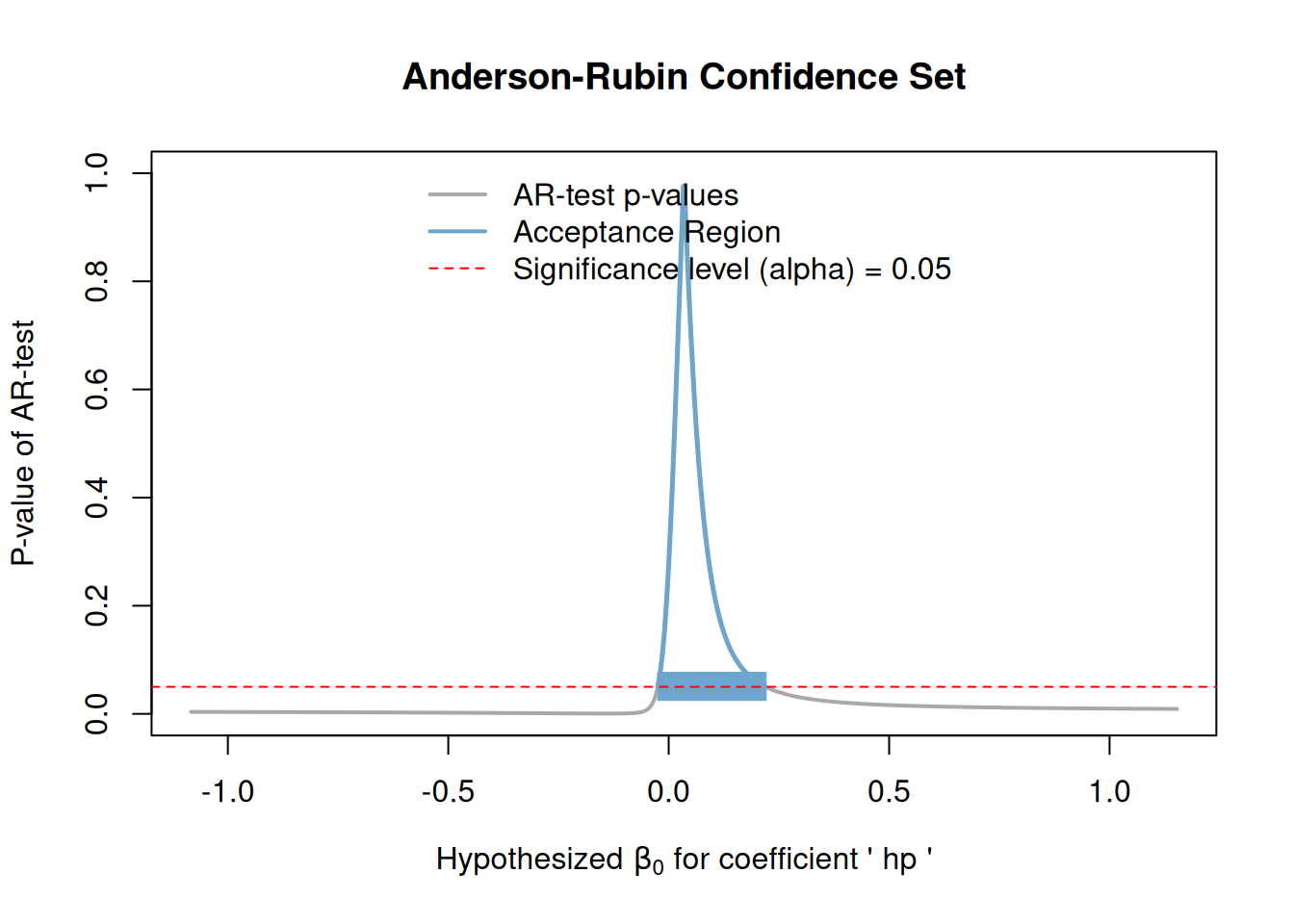

Then, we visualize the results and extract the confidence intervals using the get_ar_ci function.

Finally, we use get_ar_ci to extract the computed confidence intervals in a tidy format.

library(fixest)

regression <- feols(mpg ~ cyl | hp ~ qsec, data = mtcars)

etable(regression)

#> regression

#> Dependent Var.: mpg

#>

#> Constant 39.65*** (3.115)

#> hp 0.0347 (0.0373)

#> cyl -3.983** (1.251)

#> _______________ ________________

#> S.E. type IID

#> Observations 32

#> R2 0.73733

#> Adj. R2 0.71921

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

arci_results <- ar_ci(regression, param = "hp", level = 0.95)

print(arci_results)

#> Anderson-Rubin95%Confidence Set for 'hp'

#>

#> The confidence set is the union of the following interval(s):

#> [-0.0247, 0.2193]

plot(arci_results)

get_ar_ci(regression)

#> [1] "[-0.025, 0.219]"